Medicare can feel overwhelming — Part A, B, C, D, supplements, enrollment windows. Jeff and Suzanne Janosick are independent Medicare agents serving Northern Kentucky and Cincinnati, here to help you find the right plan for your needs and budget — at no cost to you.

Plain-English guides to help you get your footing — wherever you are in the process.

Here's everything you need to know about your timeline, your choices, and how to avoid penalties.

A step-by-step walkthrough of when and how to enroll — whether you're retiring or still working at 65.

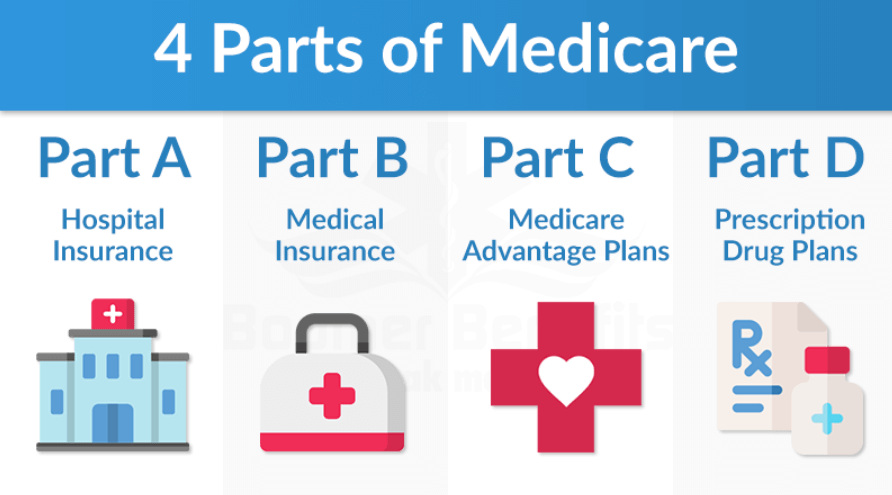

Parts A, B, C, and D explained simply — what each one covers and how they fit together.

From Medicare Savings Programs to smart plan choices — practical ways to lower what you pay.

Turning 65 is one of the most important Medicare milestones. Your Initial Enrollment Period is a 7-month window — 3 months before your birthday month, the month itself, and 3 months after. Enrolling on time matters, since missing it without other coverage can mean permanent late penalties. Here are your three main paths:

Parts A & B paired with a Medicare Supplement (Medigap), which covers the costs Original Medicare doesn't — deductibles, copays, and coinsurance. You can see any doctor in the country who accepts Medicare, with no networks or referrals. Best if you want maximum flexibility. Plan G and Plan N are the most popular in Kentucky and Ohio.

An all-in-one alternative to Original Medicare from private insurers, often bundling drug, dental, vision, and hearing coverage. Premiums are often low or even $0, though you'll typically use a network of doctors. Best if you'd rather have a single plan with potential extra benefits.

Basic hospital and medical coverage paired with a standalone Part D prescription drug plan, often combined with a Supplement for fuller coverage. Part D plans vary a lot in which drugs they cover and at what cost — so the right one depends on your specific medication list.

Limited income or assets? You may qualify for a Medicare Savings Program — a Kentucky or Ohio state program that can help pay your Part B premium, deductibles, and copayments. We can help you find out if you qualify.

Real people, real coverage, real peace of mind. Here's what our clients across Northern Kentucky and Cincinnati have to say about working with MedMyWay.

Your IEP is a 7-month window built around your 65th birthday — and it's the most important deadline in Medicare. Get it right and your coverage starts smoothly. Miss it without other qualifying coverage, and you could face late-enrollment penalties that stick with you for life.

The good news? You don't have to track it alone. Jeff and Suzanne help you map out your exact dates, compare your options, and enroll on time — so nothing slips through the cracks.

Your enrollment window opens. This is the ideal time to enroll — sign up now and your coverage will be active the very first day you turn 65, with no gap.

The month you turn 65 sits at the center of your window. If you haven't enrolled yet, coverage you sign up for this month still starts promptly — but earlier is always smoother.

Your window closes at the end of this period. It's your last chance to enroll without risking a permanent Part B late-enrollment penalty — so don't let it pass.

When you work directly with an insurance company, you only see their plans. When you work with MedMyWay, you see everything. As independent Medicare agents, Jeff and Suzanne are contracted with every major Medicare carrier in Northern Kentucky and Cincinnati — which means you get an unbiased comparison of every plan available in your area, not just the ones from a single company.

And because Medicare carriers compensate agents directly, our guidance is completely free to you. The premium you pay is identical whether you work with MedMyWay or enroll on your own.

Whether you're turning 65, reviewing your current coverage, or just not sure you're in the right plan — we'll walk you through your Medicare options across every carrier we represent. No pressure, no jargon, and no cost to you. Let's find coverage you can feel good about.